You'll be re-directed to the Financial Professional site.

EXECUTIVE SUMMARY

At Dodge & Cox, we believe the key investment risks are the possibility of permanent loss of capital and erosion of future purchasing power. Our principal tasks are to find investments with attractive risk-adjusted returns and to build portfolios that provide long-term value for our clients. This involves recognizing the potential drivers of the risk of a long-term loss of capital as well as the return premium for taking that risk. By developing substantial knowledge about each holding, and analyzing overall portfolio risk exposures, we seek to manage risk effectively and to help our clients achieve their long-term investment objectives.

We encourage our investors to focus on long-term returns and risk statistics. In our view, longer-term risk statistics provide a more accurate assessment of risk for active, fundamental, value-oriented investment managers like Dodge & Cox because such measures more closely match our long-term investment horizon.

UNDERSTANDING RISK

Risk and return are the yin and yang of investing, intricately interwoven and inseparable. The returns investors receive represent compensation for accepting risks. Investors face the crucial tasks of determining the level of risk they are willing and able to assume and then seeking attractive returns within that context.

While return and risk are fundamental investment concepts, very different approaches are required in their estimation. Returns can be calculated using widely accepted methodologies and based on publicly available numbers, such as closing prices of a security. To be sure, there are sometimes complexities in valuing assets that are not publicly traded or that trade infrequently. But ultimately returns can readily be compared across portfolios and time periods.

Risk measurement, however, is much more complicated. There are many frameworks for describing investment risk. They differ in the way they incorporate the probability of events occurring in the future. They also make different assumptions about the investment objective and time horizon.

We believe the central investment risks are the possibility of permanent loss of capital and erosion of future purchasing power. Therefore, our risk analysis is primarily focused on thoroughly understanding each security relative to its long-term prospects. Risk statistics that measure variation in short-run returns, like volatility and tracking error(a) versus a benchmark, are a secondary concern. In fact, we believe that excessive emphasis on the short term can not only be distracting, but more importantly, may impair long-term investment results.

OUR RISK MANAGEMENT APPROACH

At Dodge & Cox, risk management begins at the individual security level and integrates an overarching examination of the portfolio. Our approach to mitigating investment risk is characterized by the following attributes:

- Intensive bottom-up research with a focus on valuation. Individual security selection drives the investment process for the Dodge & Cox portfolios. We undertake extensive research on individual companies and securities to find solid investments whose true long-term value has not yet been recognized by the market. This oftentimes means we need to wait for the value we have perceived to be realized. While the price at which we sell a security is very important, the price at which we buy it is equally important.

- Analysis of overall portfolio risk exposures. Our investment committees carefully consider risk at the portfolio level. We analyze the combination of independent risk exposures to determine whether they are likely to diversify or magnify the portfolio’s overall risk profile.

- Long-term investment horizon. We evaluate each potential investment based on a three- to five-year investment horizon, and view ourselves as investors in companies and other securities rather than traders of abstract pieces of paper. That means we need to develop a deep understanding of an investment in order to formulate a view on its future prospects. And that can only be done through fundamental research, coupled with a long-term horizon.

ASSESSING INVESTMENT RISK THROUGH BOTTOM-UP COMPANY RESEARCH

In order to develop a thorough understanding of each investment we make, our analysts monitor publicly available information and talk to management to take the measure of the company’s leaders and better understand their long-term strategy. They often visit a company’s facilities and talk to vendors, customers, competitors, and industry experts.

Our goal is to develop a complete picture of a company: What are its competitive position and prospects? Where are revenues and earnings headed? What are the prospects for cash flow generation and management’s priorities for use of cash flow? What are the company’s strengths and weaknesses? Our analysts create scenarios and model the financial results the company might generate in various circumstances. While they are very interested in the upside potential for a company, they are also focused on the downside: What could go wrong? How well positioned is the company to withstand various challenges? What are the likely consequences of various kinds of bad news on the price of a company’s shares and bonds?

Following rigorous research and due diligence, our analysts present their findings in thorough written reports and make formal recommendations to our investment committees regarding specific securities to buy and sell. Moreover, since their research is ongoing, analysts may also propose additions or reductions to existing holdings as company fundamentals and valuations shift.

Our investment committees are composed of senior portfolio managers and experienced analysts. Our team- based approach provides checks and balances, tests our conviction, and broadens our knowledge base over time. In group deliberations, the focus on an investment’s total return potential is balanced by an examination of its risks.

Valuation Is Critical

At Dodge & Cox, we do not simply look for investments with attractive long-term fundamentals; we look to buy them at the right price. Starting valuations are significant drivers of long- term returns (i.e., greater price discounts to fundamental value are associated with higher returns). The wider the margin between the price we pay and our estimate of the security’s fundamental value, the more likely we are to earn a positive long-term return.

We often favor companies with low expectations where we believe the risks and challenges are already incorporated into the market price of their securities. These valuations often reflect concerns about a company’s future earnings and cash flow prospects that our analysts believe are overly pessimistic or do not reflect the management’s degrees of freedom.

For equities, the companies we invest in typically trade at or below average valuations as measured by a variety of metrics, including price-to-earnings ratios, price-to-sales, and multiples of book value, cash flow, and asset values. We do not rely on any single measure or formula in looking at valuation; rather we consider an array of valuation metrics to guide our selections. For corporate fixed income securities, the issues we invest in offer attractive interest rate spreads and structural protections relative to our assessment of their credit risk.

Reviewing, Revisiting, Rebalancing

Recognizing that it is impossible to time the bottom or top of a company’s share price, we are patient and often move incrementally as we revisit and retest our thinking. While we approach our investments from the long-term perspective of being a part owner of a business, we constantly monitor each investment and often take advantage of short-term price volatility, after incorporating any new developments with the company, industry, or market environment. Changes in valuation in the short run provide opportunities to adjust our position sizes, reflecting our updated views on long-term returns and relative value among our portfolio holdings.

MANAGING OVERALL PORTFOLIO RISK

Portfolio construction is largely the result of bottom-up investment decisions. However, our investment committees carefully consider risk at the portfolio level. We analyze whether the combination of independent risks will diversify or magnify the portfolio’s risk exposures.

Occasionally, we are comfortable taking a more concentrated exposure because the market may be offering an attractive premium to investors willing to take the exposure. Examples would include being overweight a particular sector (e.g., Health Care) or having meaningful exposure to emerging markets, which is discussed in the sidebar. More typically, our analysts highlight the external factors that may affect the investment outcome, and we try to balance these risks against the potential rewards. To manage risk exposure at the portfolio level, our investment committees pay particular attention to portfolio diversification and our quantitative estimates of aggregate risk.

Quantitative Estimates of Aggregate Risk

The long-term profitability of any company will be driven by the combination of its internal business decisions and its external economic environment. We combine quantitative and qualitative techniques to understand how each holding’s return drivers may affect the overall portfolio.

Internal business decisions are generally company specific, with a limited impact on a diversified portfolio. Position sizing and knowledge of corporate strategy provide our investment committees with an understanding of the portfolios’ company-specific risks. We will also refer to quantitative analytics to identify the most important company-specific exposures in the portfolio.

The impact of external economic variables can be more pervasive as commodities, currencies, interest rates, and other external factors affect the success of a large number of individual companies across global regions and economic sectors. These risks generally concentrate rather than diversify.

The relationships are not always obvious. For example, HP Inc.(b) (formerly Hewlett-Packard) has a notable exposure to the Japanese yen. This may be surprising for a U.S.-domiciled company that has only a small percentage of its sales in Japan. An understanding of its business environment, however, reveals that its chief competitors are Japanese companies with costs and prices in Japanese yen. A stronger yen pressures its competitors to raise prices in the printing industry, which could allow HP’s profit margins to rise. As we consider how foreign exchange rates affect a portfolio’s investments, we need to consider the Japanese yen impact from HP just as much as the Japanese yen impact from a holding with significant sales in Japan.

In order to quantify these relationships in the Dodge & Cox portfolios, we use internal and third-party risk models. We find our internal models are particularly helpful in understanding the risks of our equity portfolios. For every stock in our investment universe, we use statistical techniques that attempt to capture robust

relationships between economic variables and the long-term stock price return. Our portfolio strategy team discusses company-level exposures with our global industry analysts and aggregates these exposures at the portfolio level for our investment committees.

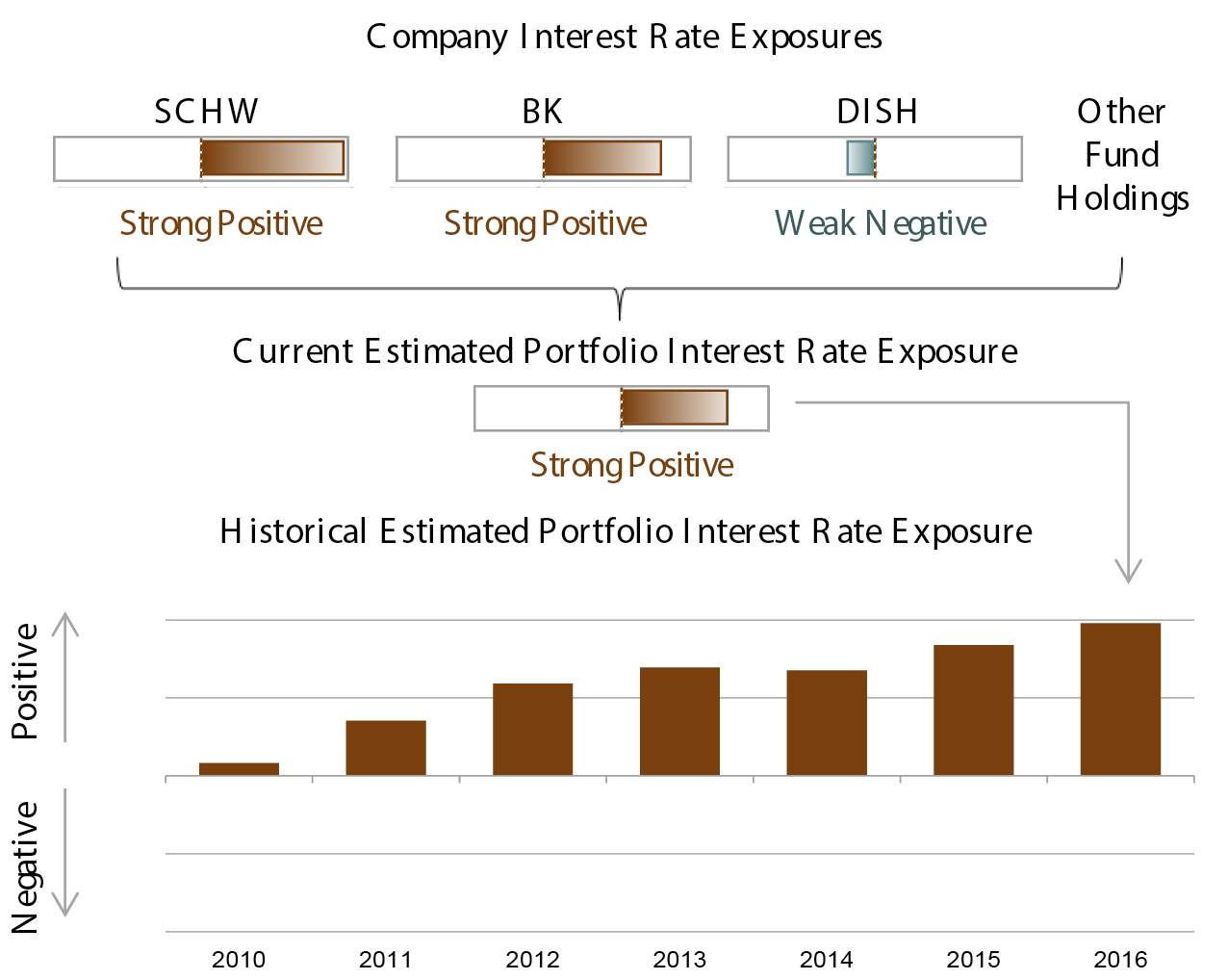

For example, we have found that exposure to long-term U.S. interest rates is a key differentiator between the exposures of the holdings of the Stock Fund and the constituents of the S&P 500. As is shown in the chart to the right, at the company level, we estimate a number of the Fund’s equity holdings (e.g., Charles Schwab, Bank of New York Mellon) would show strong positive performance with an increase in long-term interest rates; this is not fully offset by other holdings, like Dish Network, that we estimate would perform slightly worse with rising interest rates.

Having identified and estimated the portfolio’s key economic exposures, our investment committees consider three key questions:

1. Are these exposures an intentional part of our investment thesis or an unintended aggregation of unwanted risk? 2. What risk premium(c) is embedded in this exposure?

3. Is the magnitude of the exposure appropriate for the portfolio?

While our focus is on bottom-up security analysis, our investment committees also consider the resulting aggregate risks in the portfolios. In some cases, the market pricing of a risk exposure creates an attractive long-term return opportunity. This is precisely the reason why the U.S. Equity Investment Committee managing the Dodge & Cox Stock Fund became comfortable with the portfolio’s exposure to rising interest rates (highlighted in the chart on the previous page). Our research suggested that we were being well compensated through significantly discounted company valuations to take interest rate exposure. As our analysts modeled companies like Charles Schwab and Bank of New York Mellon, the asymmetric benefit from rising interest rates was a part of each company’s investment thesis. In contrast, our analysts could not find compelling investment opportunities among the stocks that benefited from declining rates, like electric utilities. Our review of aggregate portfolio exposures confirmed that stocks with exposure to rising rates offered an unusually large risk premium.

We have found that the combination of systematic data analytics with the company expertise from our industry analysts provides our investment committees with powerful tools for understanding and managing portfolio risk.

SEPARATING THE SIGNALS FROM THE NOISE: THE LONG-TERM PERSPECTIVE

Decades of investing have taught us that security prices often fluctuate much more widely than the underlying fundamentals. It is difficult if not impossible to predict short-term price movements. As Benjamin Graham, the celebrated champion of value investing, famously noted: in the short term, markets are voting machines, reflecting the constantly shifting opinions of investors, but in the long term the markets are weighing machines, ultimately reflecting a company’s true earnings. We focus on the long term.

Day-to-day fluctuations in investment prices may reflect important developments in the life of a company—but they can also reflect false alarms, a rush to judgment, or irrational exuberance. It is important to separate the signals from the noise. And in seeking to do that, investors are best served by matching their risk horizons and their return horizons. When short-term returns are used to evaluate investment risk, price fluctuations can produce misleading signals regarding volatility and risk. On some days, the sound and fury in the market may signify nothing. Relying on longer periods of time over which to analyze investments provides a more accurate and meaningful assessment of risk. Our task is to identify the long-term investment opportunities that are to be found amid the constant motion in the markets.

It is interesting to note that when calculating risk statistics, monthly returns can generate substantially different values than return increments of a year or more. This is true for both equity market beta and realized volatility measures. Our analysis suggests active investment strategies based on fundamental value exhibit lower risk characteristics when returns are measured over longer horizons because shorter measuring periods typically overstate longer-term risk.(d)

The Dodge & Cox Stock Fund as an Illustrative Example

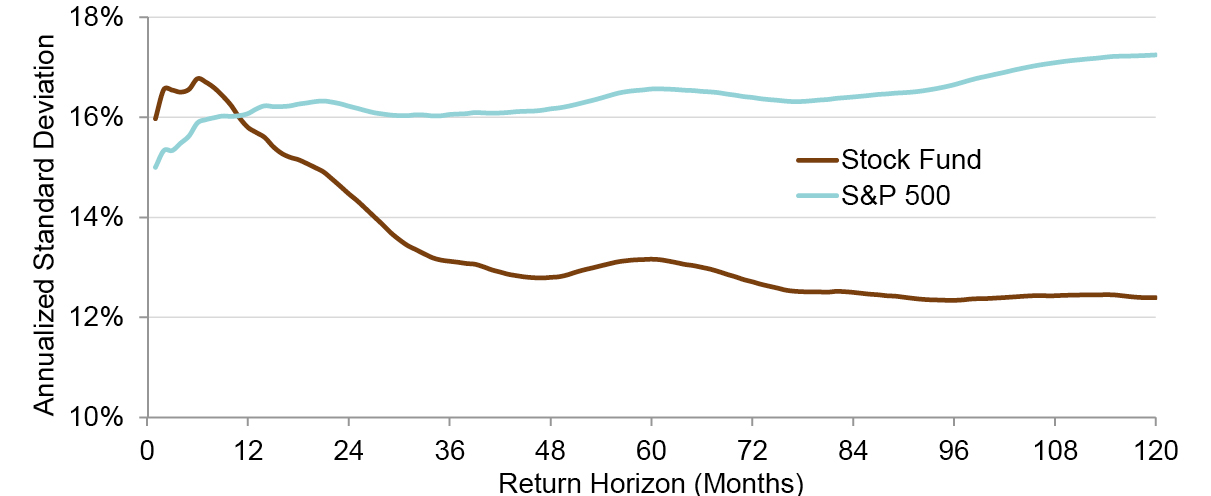

Risk statistics are affected significantly by the choice of daily, monthly, or annual returns. Below we show volatility calculations for the Stock Fund versus the S&P 500 for return horizons ranging from one month to ten years.

In our view, short-term return volatility is a poor measure of long-term risk.(e) As is shown in the chart to the right, the annualized volatility of the Stock Fund declines significantly when measured over longer return horizons. Using one-month return increments, annualized volatility was 15.9% for the Stock Fund versus 14.9% for the S&P 500 over the last 50 years. However, for return horizons longer than three years, the volatility of the Stock Fund declined to less than 13% per year, while the volatility of the S&P 500 increased to approximately 16% per year.

Why might the Stock Fund’s long-term risk be lower than is indicated by short-term measures? As long-term investors with a three- to five-year investment horizon, we concentrate our research on company fundamentals that drive intrinsic value and aim to deemphasize temporary factors that influence short-term price volatility.

Sources: Dodge & Cox, Standard & Poor’s.

IN CLOSING

Risk management is an essential element of portfolio management. Our clients trust us to wisely invest their assets in an uncertain world. By becoming experts in each holding, understanding how their risks aggregate at the portfolio level, and focusing on the long term, we seek to minimize the risk of a permanent loss of capital while growing long-term purchasing power.

Disclaimer

Data has been obtained from sources considered reliable, but Dodge & Cox makes no representations as to the completeness or accuracy of such information. Opinions expressed are subject to change without notice. Before investing in any Dodge & Cox Fund, you should carefully consider the Fund’s investment objectives, risks, and charges and expenses. To obtain a Fund’s prospectus and summary prospectus, which contain this and other important information, visit dodgeandcox.com or call 800-621-3979. Please read the prospectus and summary prospectus carefully before investing.

1 Tracking error is a measure of how closely a portfolio follows a benchmark. It is the standard deviation of the difference between the portfolio and benchmark returns over time.

2 The use of specific examples does not imply that they are more attractive investments than other holdings. Holdings referenced are as of March 31, 2017.

3 The risk premium represents the additional return investors expect to earn to compensate them for a security’s risk.

4 Statistically, this can be thought of as a test for autocorrelation. All else equal, a time series with lower (or more negative) autocorrelation will have lower long-term volatility. Our prediction can therefore be expressed as the claim that the returns of value investors show lower autocorrelation than the returns of index funds.

5 Annualized volatility is the standard deviation of log monthly returns scaled by the square root of (12/n), where n is the number of months in the return horizon.