You'll be re-directed to the Financial Professional site.

Key Takeaways

- Concerns about the impact of the global coronavirus (COVID-19) pandemic have roiled financial markets. Stock prices of European and UK Financials have declined substantially, stemming from fears about the depth and duration of the downturn in the real economy and its impact on the near-term prospects for financial services companies.

- In contrast to the global financial crisis (2008-09) and European sovereign debt crisis (2011-12), we believe that the probability of permanent loss of capital (e.g., through liquidity/funding shortfalls or large dilutive capital raises) is low given the combination of stronger bank balance sheets, regulatory easing, and accommodative fiscal measures.

- Conversely, current valuations are below prior crisis levels and imply structural impairment of the long-term earnings power of these companies, which we believe is overly pessimistic. While the economic downturn will hurt their near-term profitability, we believe that European and UK Financials with strong underlying fundamentals will be resilient during the current crisis and achieve higher profitability longer term. Even returning to 2018/2019 profitability levels (which banks had previously been targeting improvements upon) over the next three to five years could generate significant upside.

- Dodge & Cox Worldwide Funds—U.S. Stock Fund and Global Stock Fund are overweight European and UK Financials. We have strong conviction in these holdings and believe their long-term risk-reward profiles are compelling at current valuation levels.

Context

COVID-19 has evolved into a global pandemic that has disrupted all major economies, increased financial market volatility, and caused equity markets across the globe to decline precipitously. Stock prices of financial services companies have declined disproportionally. In the MSCI ACWI Index, Financials were down 32% compared to down 21% for the overall Index during the first quarter of 2020.

The public health responses designed to slow the spread of COVID-19 have led to a dramatic reduction in economic activity around the world. Policymakers have responded with substantial amounts of fiscal and monetary stimulus, and the global scientific community is aggressively working on COVID-19 treatments and vaccines. Compared to the 2008-09 global financial crisis, the current crisis is medical in nature rather than one stemming from problems in the banking system. Banks entered this crisis in much stronger financial shape, which in our view makes them well positioned to help serve as part of the solution to the pandemic’s economic impact.

We Have Stress Tested the Fund's Holdings

Our global industry analysts continue to have frequent discussions with management teams and industry experts to gauge downside risks and current operating conditions. In addition, they have continued to work closely with our fixed income credit analysts to stress test the Funds’ European and UK Financials holdings1 at extreme conditions, including negative benchmark yields, credit losses similar to those experienced during the global financial and European sovereign debt crises, large equity market drawdowns, and significant declines in investment banking and trading revenue. Furthermore, we have examined the economic impact of past disease outbreaks to understand various possible economic outcomes.

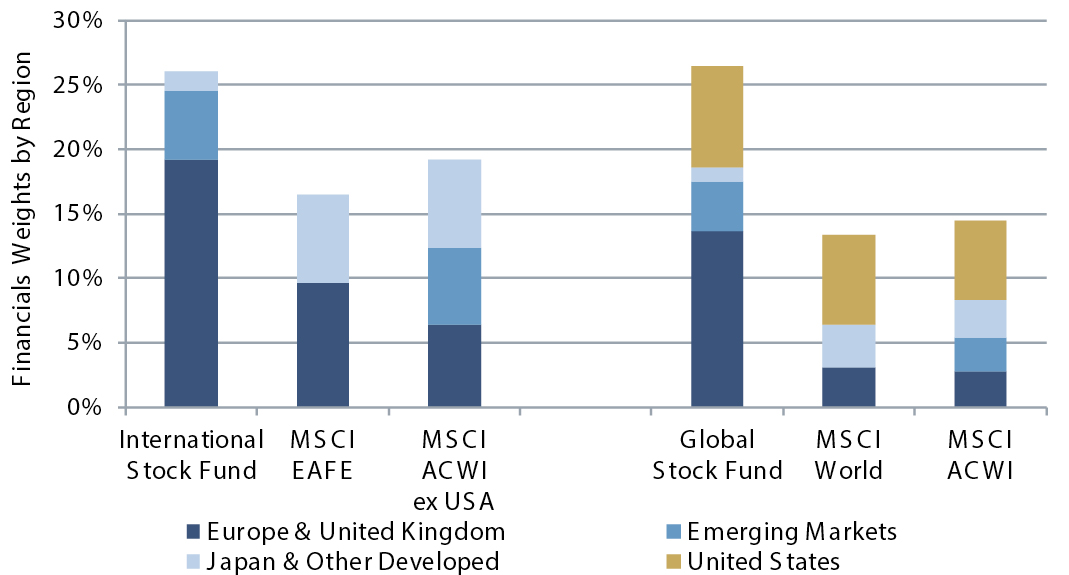

We model a wide range of scenarios to 1) understand if the Funds’ holdings can adequately withstand short-term credit and interest rate pressures (“play defense”) and 2) compare what current valuations imply versus our forecasted long-term fundamentals to evaluate if we are presented with an attractive risk-adjusted return opportunity (“play offense”). Our ongoing due diligence leads us to believe that the Funds’ European and UK Financials holdings have sufficient capital and liquidity to weather the current storm. The International Stock Fund and Global Stock Fund remain overweight European and UK Financials (shown in Figure 1).2

Figure 1: Funds Are Overweight European and UK Financials

Source: MSCI via FactSet.

Improved Balanced Sheets Provide Downside Mitigation

Over the past decade, fundamentals have improved across the Funds’ current European and UK Financials holdings, driven by management actions to bolster balance sheets, build capital, and increase profitability. In particular, balance sheets are far more resilient today.

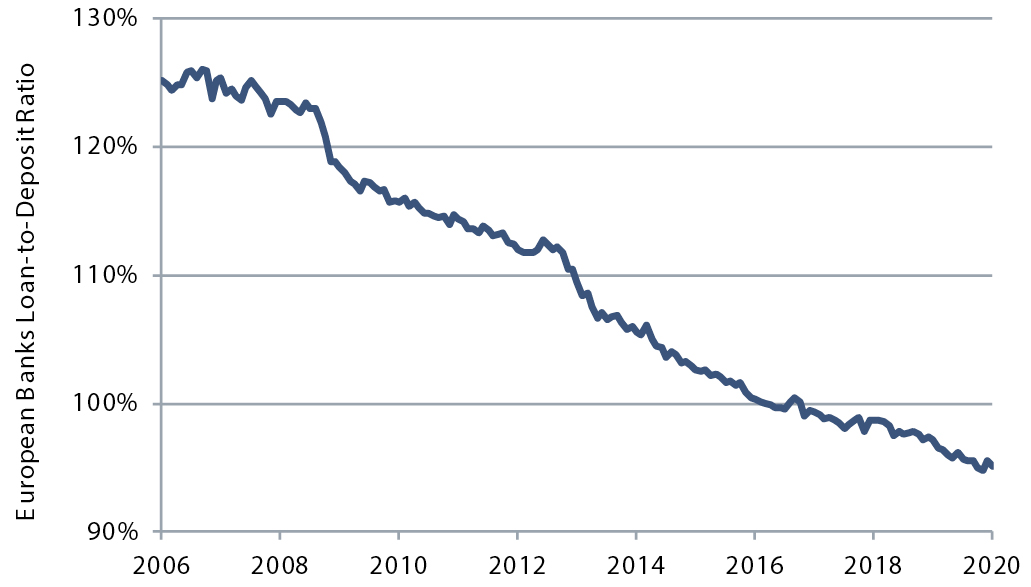

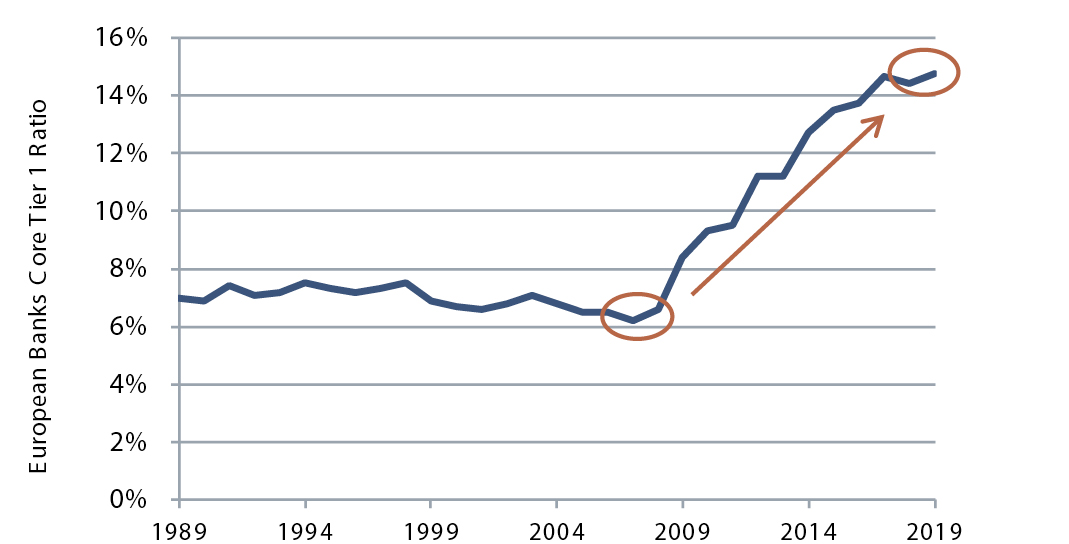

As illustrated in Figure 2, funding models have substantially improved as loan-to-deposit ratios have declined and more stable customer deposits have replaced short-term wholesale funding. In addition, capital levels have more than doubled over the last decade (see Figure 3), driven by tighter regulatory standards. Strong balance sheets are a critical source of downside mitigation for investors, as they reduce the probability of permanent loss of invested capital (e.g., through liquidity/funding shortfalls or large dilutive capital raises).

Figure 2: Funding Models Have Vastly Improved

Source: J.P. Morgan Equity Strategy, European Central Bank.

Figure 3: Capital Ratios Have More Than Doubled3

Source: European Central Bank.

Furthermore, European private sector credit growth has been close to zero over the last decade. Low interest rates have been used to reduce private sector leverage and support debt serviceability, which in turn have enabled banks to improve their asset quality and reduce non-performing loans. While credit losses will almost certainly increase due to the recessionary impact of COVID-19, banks are entering this period after a decade of risk reduction. This is in stark contrast to the global financial crisis, which banks entered on the back of rapid credit expansion that drove subsequent large losses.

Unprecedented Fiscal, Monetary, and Regulatory Responses

To date, regulators and government agencies have taken unprecedented measures to support the banking system in order to ensure continual supply of credit to the economy.

Fiscal policy: Governments across Europe have created large fiscal stimulus plans to mitigate the impact of COVID-19 on the economy. In addition to providing direct payments to individuals and enabling loan service holidays, the fiscal measures include support for corporations and small-to-medium sized enterprises (SMEs) through government-guaranteed loan programs that will be intermediated by the banks. While the magnitude of the programs and credit guarantees vary by country, they create a critical credit loss-sharing mechanism between banks and government.

Monetary policy: European and UK central banks have expanded their asset purchase programs and are providing long-term loans to banks at very cheap rates. For example, the European Central Bank has increased its long-term refinancing operation program from 30% of banks’ loan books to 50% and is charging a negative 75 basis points4 interest rate for it.

Regulatory policy: European and UK bank regulators have temporarily reduced banks’ capital and liquidity requirements, and are allowing banks to fill a part of their capital requirements with junior debt instruments instead of common equity. In addition, they have postponed 2020 stress tests and guided banks to use qualitative overlays to dampen pro-cyclical accounting rules. In exchange, banks have been asked to temporarily halt dividends and share repurchases until October 1, 2020. This accommodative behavior and flexibility on behalf of regulators differs drastically from prior downturns; in past crises, banks were forced to issue large amounts of equity as regulatory standards tightened.

The Opportunity: Compelling Valuations Relative to Longer-Term Earnings Power

Current European bank valuations are below prior crisis levels at 0.4 times book value and imply structural impairment of banks’ earnings power. We believe this is overly pessimistic.

Figure 4: Historically Low Valuations

Source: FactSet financial data and analytics.

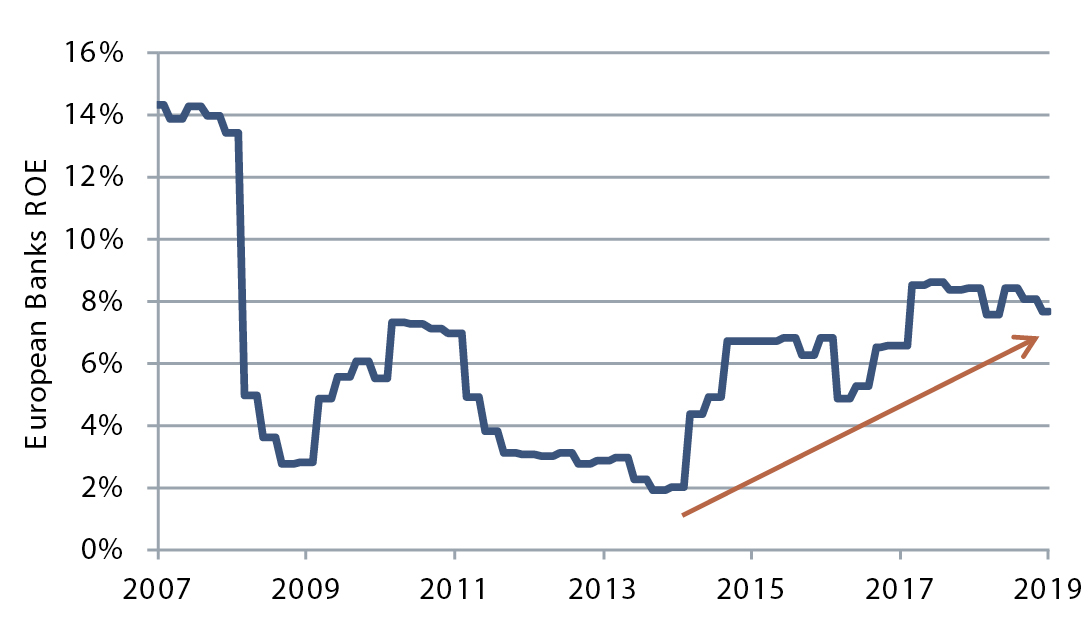

Over the past 12 years, European and UK financial institutions have operated in a very challenging context including the global financial crisis, European sovereign debt crisis, the United Kingdom’s exit from the European Union (Brexit, finalized January 2020), and an environment of slower economic growth, prolonged low interest rates, and political uncertainty. Furthermore, capital requirements more than doubled during this period as regulatory standards tightened. The Funds’ current European and UK bank holdings have survived these “real life” stress tests, and have subsequently been improving profitability along with other European banks, as shown in Figure 5.

Figure 5: Improved Return on Equity

Source: FactSet financial data and analytics.

In 2018-2019, European banks earned an average return on equity (ROE) of approximately 8% despite operating in a backdrop of low economic growth and negative interest rates. Prior to the onset of COVID-19, the management teams of the Funds’ bank holdings were targeting an improvement in ROE to 10% on average, largely through self-help measures such as cost cutting, exiting low-return sub-scale business lines, and further shifting their business models towards fee-generating businesses that consume less capital. In addition, they have been investing heavily in technology to meet their customers’ evolving digital banking needs and streamlining middle- and back-office functions.

While the economic downturn caused by COVID-19 will hurt near-term profitability of many financial institutions, we believe those impacts will likely be transitory for those that have strong underlying fundamentals. Even returning to 2018/2019 profitability levels over the next three to five years could generate upside from current valuation levels. Resumption of capital return in the form of dividends and share repurchases would add another pillar of support to valuation. While we continue to assume a prolonged slow growth and low interest environment, we believe an improvement in the macroeconomic backdrop over the long term, coupled with achieving longerterm management targets, has the potential to drive further upside.

Finding Value Through Individual Security Selection

Our portfolio construction continues to be driven by rigorous bottom-up analysis and individual security selection. The Funds’ European and UK Financials investments are diversified across business models and geographies. Below we highlight two of the Funds’ larger European bank holdings to illustrate how we look beyond macro concerns to unearth long-term value opportunities.5

Banco Santander

Banco Santander is a Spain-domiciled European bank with large businesses in Spain, the United Kingdom, and Brazil. While Banco Santander will face economic headwinds from COVID-19, the bank trades at 0.4 times book value and six times trailing earnings, an inexpensive valuation given its attractive long-term fundamentals. In our view, Banco Santander is one of the better-run European banks with high pre-provision profit levels, which provides a cushion to absorb credit losses beyond regulatory and government measures. The bank remained profitable through the global financial and sovereign debt crises, and in addition to its defensive characteristics, has attractive long-term growth prospects through its emerging markets footprint. Furthermore, senior management has high equity ownership and is aligned with long-term shareholders.

UBS Group

Based in Switzerland, UBS is the world’s largest private bank and wealth manager. At 0.6 times book value, UBS is trading at its lowest valuation since the global financial crisis despite being in a much stronger financial position. Capital levels are also higher. In recent years, management has repositioned the company's business mix towards wealth management and reduced its risk profile. UBS has the premier brand, scale, and footprint in wealth management with a particular strength in Asia. While UBS will face headwinds from lower market asset levels and interest rates, we believe the company’s profitability will remain robust.

In Closing

Our deep fundamental research often gives us the conviction and confidence to invest when companies and sectors are out of favor, as is currently the case with European and UK Financials. We remain enthusiastic about the long-term outlook for the Funds’ European and UK Financials investments. While the economic impact of COVID-19 is uncertain and we continue to stress test these holdings, we observe that these companies are far more resilient today than they were in previous periods of economic stress. Furthermore, the accommodative fiscal, monetary, and regulatory responses to COVID-19 are large and unprecedented, which should help to mitigate downside risk.

Current valuation levels imply structural impairment of the long-term earnings power of these companies, which we believe is overly pessimistic. While the economic downturn will hurt their near-term profitability, we believe that European and UK Financials with strong underlying fundamentals will be resilient during the current crisis and achieve higher profitability longer term. Even returning to 2018/2019 profitability levels over the next three to five years, coupled with resumption of capital return, could generate significant upside. An improvement in the macroeconomic backdrop over time, especially higher interest rates, would be a further tailwind.

Patience and persistence are essential to long-term investment success. We encourage our clients and shareholders to take a similar view. Thank you for your continued confidence in Dodge & Cox.

Disclosures

This information should not be considered a solicitation or an offer to purchase shares of Dodge & Cox Worldwide Funds plc or a solicitation or an offer by Dodge & Cox Worldwide Investments and its affiliates to provide any services in any jurisdiction. The views expressed herein represent the opinions of Dodge & Cox Worldwide Investments and its affiliates and are not intended as a forecast or guarantee of future results for any product or service. To obtain more information about the Funds, please refer to the Funds’ prospectus at dodgeandcoxworldwide.com.

The above information is not a complete analysis of every material fact concerning any market, industry, or investment. Data has been obtained from sources considered reliable, but Dodge & Cox makes no representations as to the completeness or accuracy of such information. Opinions expressed are subject to change without notice. The information provided is historical and does not predict future results or profitability. This is not a recommendation to buy, sell, or hold any security and is not indicative of Dodge & Cox’s current or future trading activity. Any securities identified are subject to change without notice and do not represent a Fund’s entire holdings.

The MSCI World Index is a broad-based, unmanaged equity market index aggregated from 23 developed market country indices, including the United States and Canada. The MSCI ACWI (All Country World Index) Index is a broadbased, unmanaged equity market index aggregated from 46 developed and emerging market country indices. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This publication is not approved, reviewed, or produced by MSCI.

The Dodge & Cox Worldwide Funds—Global Stock Fund is subject to equity risk and market risk, meaning investments in a Fund can be volatile and may decline in value because of changes in the actual or perceived financial condition of their issuers or other events affecting their issuers. Investment prices may increase or decrease, sometimes suddenly and unpredictably, due to general market conditions. Local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issue, recessions, or other events could also have a significant impact on a Fund and its investments. In addition, investing in securities may entail risk due to economic and political developments; this risk may be higher when investing in emerging markets.

Endnotes

1 As of 31 March 2020. International Stock Fund (% of Fund’s net assets): AEGON (0.8%), Aviva (1.4%), Banco Santander (2.2%), Barclays (1.5%), BNP Paribas (2.4%), Credit Suisse Group (2.4%), Societe Generale (1.5%), Standard Chartered (1.5%), UBS Group (3.2%), and UniCredit (2.2%). Global Stock Fund (% of Fund’s net assets): AEGON (0.4%), Aviva (0.9%), Banco Santander (1.7%), Barclays (0.8%), BNP Paribas (1.8%), Credit Suisse Group (1.6%), Societe Generale (1.2%), Standard Chartered (1.3%), UBS Group (2.3%), and UniCredit (1.8%).

2 Unless otherwise specified, all weightings and characteristics are as of 31 March 2020.

3 The Common Equity Tier 1 ratio (CET1) is a measure of bank solvency that gauges a bank’s capital strength. Common Equity Tier 1 ratio = Common Equity Tier 1 Capital / Risk-Weighted Assets.

4 One basis point is equal to 1/100th of 1%.

5 The use of specific examples does not imply that they are more or less attractive investments than the portfolio’s other holdings.