You'll be re-directed to the Financial Professional site.

Key Takeaways

- Energy has performed poorly over the past ten years and was the worst-performing sector during the first half of 2020. The combination of an unprecedented fall in demand and an increase in supply has weighed most recently on the oil markets.

- Our global industry and fixed income credit analysts have thoroughly stress tested the financial models of the Dodge & Cox Worldwide Funds’ energy investments1 using various oil price scenarios. We believe these companies have sufficient capital and liquidity to weather the current storm.

- We have also conducted further due diligence on many factors, including ESG risks, for their potential to materially impact a security’s risk-reward profile.

- While oil prices are currently low, we believe they will likely increase over our three- to five-year investment horizon.

- Current energy valuations—trading at 90-year lows—are depressed and provide an attractive starting point. We continue to find compelling long-term opportunities in selected upstream and oilfield services companies with assets on the low end of the global cost curve, management teams that have deployed capital prudently through the cycle, and low-toreasonable valuations. As a result, our Investment Committees have maintained overweight positions in Energy within the Dodge & Cox Worldwide Funds. Exposure to Energy ranges between 7 to 12% of each Fund.

Simultaneous Oil Demand and Supply Shocks

Oil price downturns are typically driven by demand shocks caused by recessions or by new structural additions to supply, such as the U.S. shale surge in 2014-16 or the production glut in the early 1980s from Alaska and Mexico. Historically, supply reductions from OPEC2 have cushioned these shocks. However, the recent confluence of oil demand and supply shocks in March 2020 constituted a black swan event. Saudi Arabia’s decision to launch an oil price war—raising crude production and offering deep discounts after Russia refused to expand production cuts with OPEC—came just as the coronavirus pandemic (COVID-19) started to reduce global demand for oil. The sector also faces secular headwinds to demand. As a result, Energy was the worst-performing sector of the MSCI All Country Index during the first half of 2020, down 34% with oil prices down 38%.3

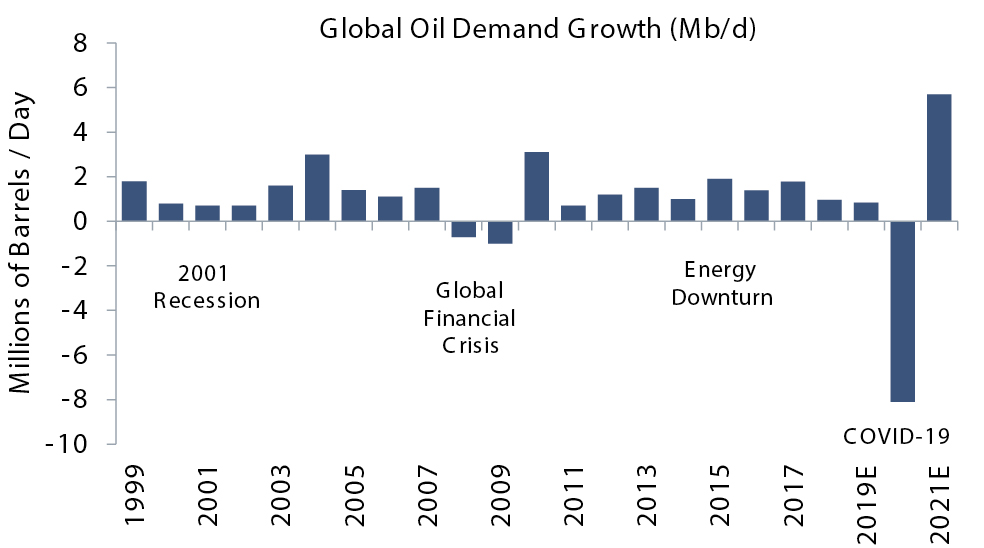

Largest Demand Decline in History

Transportation, petrochemicals, and various industrial uses are the main drivers of oil demand. In 2019, total demand was approximately 100 million barrels per day (Mbpd), with emerging markets accounting for significant demand growth.

During the first half of 2020, the public health responses designed to slow the spread of COVID-19 led to a dramatic reduction in mobility and economic activity around the world. As the virus spread globally, quarantines led to an unprecedented decline in global oil demand. After decreasing by almost 20 Mbpd in the second quarter of 2020, total global demand is estimated to fall by an average eight Mbpd for the year (see Figure 1).

Figure 1: Largest Demand Decline in History

Source: Based on IEA data from IEA (1999-2020) Oil Market Report, https://webstore.iea.org/archives, All rights reserved; as modified by Dodge & Cox.

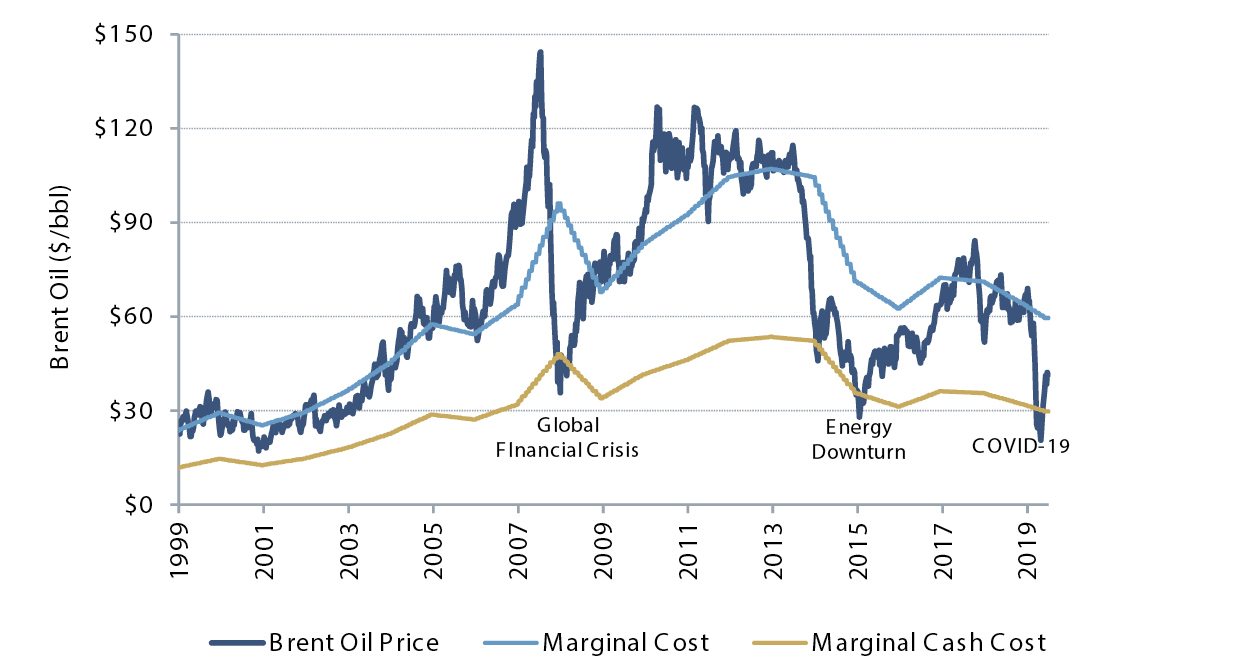

Oil Fell Below Marginal Cash Costs

Oil prices plummeted during the spring of 2020 and even became briefly negative in April as investors holding oil futures were willing to pay to offload contracts for oil they could not store. Even though oil producers around the world responded by shutting down high-cost wells and curtailing other production, the magnitude of demand destruction outweighed the reduction in supply. This imbalance between demand and supply caused prices to drop below marginal cash costs, as shown in Figure 2.

Figure 2: Brent Oil Price ($/bbl) vs. Marginal Cost

Source: Bernstein Research. Marginal cost represents the price needed to cover capital and operating expenses to bring on new oil production. Marginal cash cost represents cash operating costs, production taxes, and interest expense. Calculations are based on a global set of publicly traded oil companies.

We Have Conviction in the Funds’ Meaningful Exposure to Energy

Utilizing deep fundamental research, we seek to understand a company’s business model, competitive positioning, and financial strength in a wide variety of scenarios. This work often gives us the conviction and confidence to invest when companies and sectors are out of favor—which is currently the case with energy, where the Dodge & Cox Worldwide Funds have meaningful overweight positions (see Figure 3).

Figure 3: The Dodge & Cox Worldwide Funds Are Overweight Energy4

.jpg)

Source: Bloomberg Index Services. MSCI and S&P via FactSet.

As part of our ongoing process, we have rigorously analyzed the Funds' energy holdings and believe we have invested in companies that are well managed and have the potential to create significant shareholder value, even if oil prices do not rise. Energy valuations are inexpensive and provide an excellent starting point. While oil prices are currently low, we believe they will increase over our three- to five-year investment horizon.

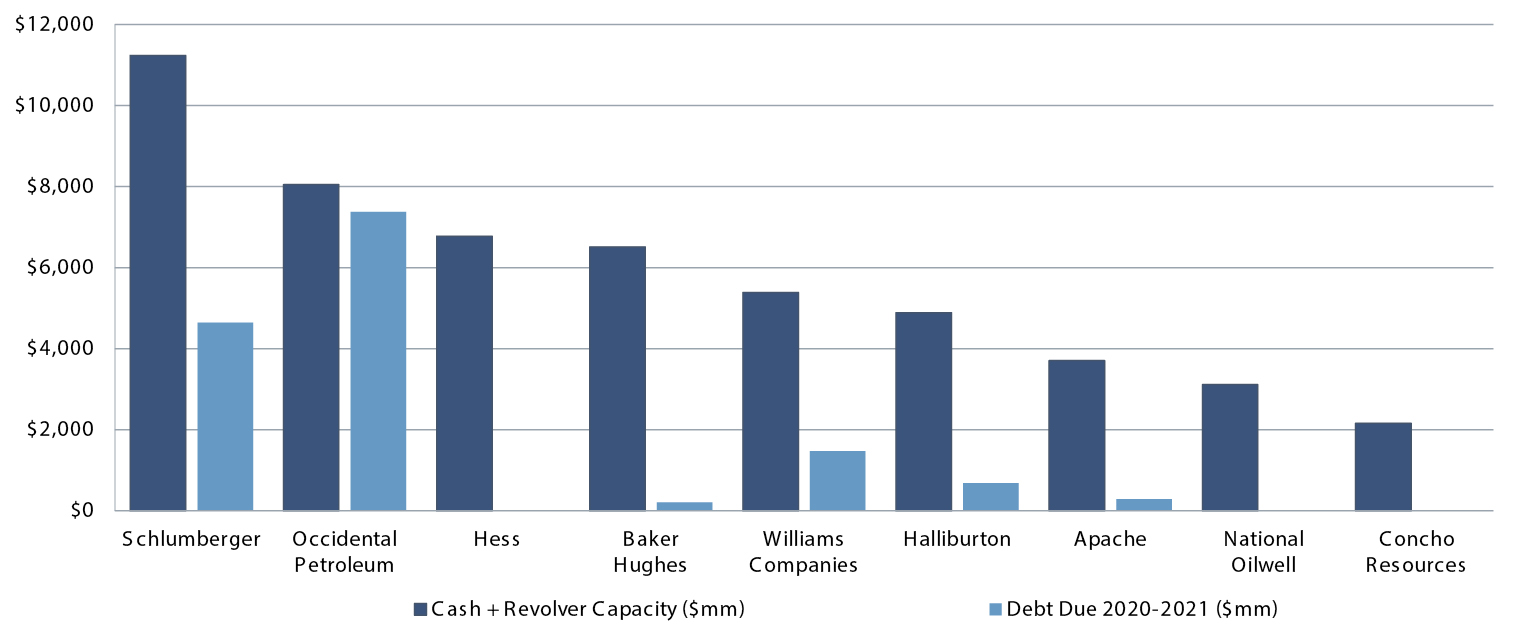

1) The Funds’ Energy Positions Generally Have Resilient Balance Sheets

Drawing on our experience during the 2008 global financial crisis and the last oil downturn in 2015-16, our global industry and fixed income credit analysts have worked closely together to stress test the Funds’ energy holdings. Collaboration between our equity and fixed income teams is a hallmark of our investment process across all stages but becomes particularly important during periods of market stress. For each energy holding, our analyst team has looked at the company’s sources and uses of cash across a variety of oil price scenarios, toggling both the severity and duration of the downturn. For companies that we expect to spend more cash than they generate (i.e., most companies in our stress case), we focus on their current sources of liquidity (e.g., cash, lines of credit) and back-up options that could be utilized to generate additional liquidity, including further reductions in capital expenditures, dividend cuts, asset sales, and debt and equity issuance. As part of these liquidity analyses, we also assessed the cost and availability of financing, eligibility for government support, the potential timing and magnitude of contingent liabilities, and impact of any debt covenants.

Figure 4: The Funds’ Energy Positions Have Resilient Balance Sheets5

Source: Source: Company reports, Dodge & Cox. Examples of Fund holdings are shown in the chart above. For a full list of the Funds’ energy investments, please reference endnote 1.

The above analysis does not exist in a vacuum. We continue to have frequent discussions with management teams, independent board members, service providers, and industry experts to gauge current operating conditions and downside risks. Our ongoing due diligence leads us to believe that the Funds’ energy holdings have sufficient capital and liquidity to survive the current headwinds, although some holdings (like Occidental Petroleum) may face larger challenges than others (like Concho Resources). Simple examples6 of current liquidity versus near-term debt maturities are shown in Figure 4.

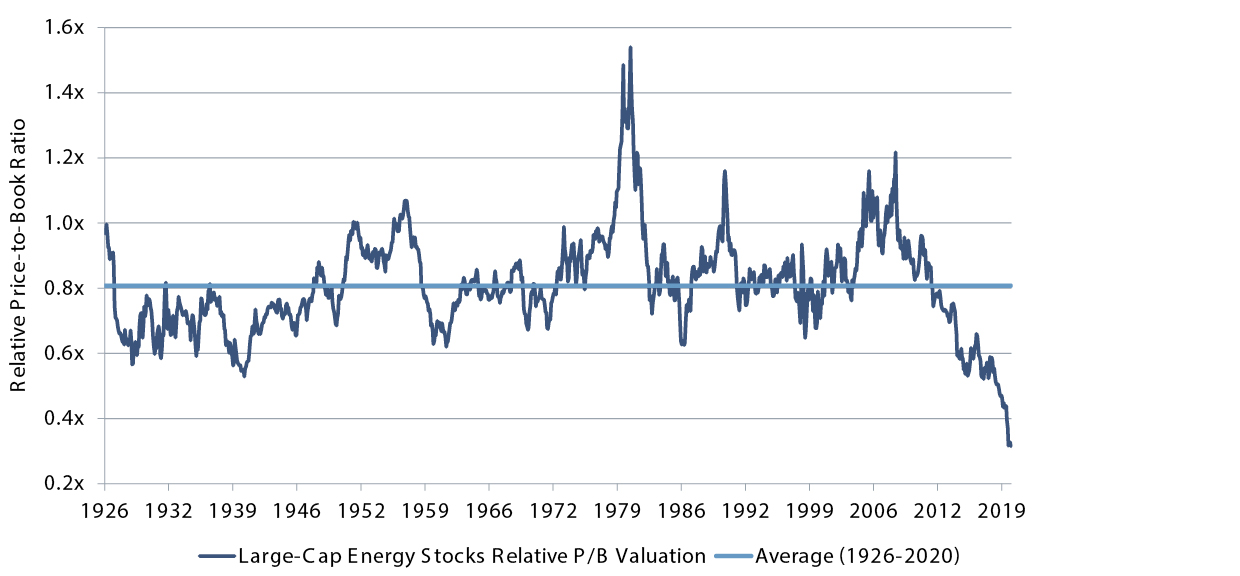

2) Energy Valuations Are at 90-Year Lows

Energy companies are currently trading at low multiples relative to history and the broader market on a price-to-book basis (see Figure 5). We believe that the fear and uncertainty dominating the headlines have driven valuations to extreme levels that already price in significant downside risks. This type of environment can create a long-term investment opportunity for value-oriented investors like Dodge & Cox. We have extensively assessed the macro environment and companyspecific risks, and believe the fundamentals of our carefully selected holdings provide an attractive starting point that more than compensates for the risks.

Figure 5: Energy Valuations Relative to the Overall Equity Market

Source: Empirical Research Partners. Capitalization-weighted data.

3) We Believe Oil Prices Will Increase Over Our Investment Horizon

The long-term outlook for oil prices is more unpredictable than usual due to demand uncertainties related to COVID-19 and multiple variables on the supply side. The typical elasticity of demand to price has broken down, as a lower fuel price alone does not stimulate more driving or flying. To model a security’s risk-reward profile, our analysts work with a range of oil price scenarios rather than a specific oil or gas price forecast.

Our global industry and fixed income credit analysts have erred on the side of conservatism, and we have used the following oil price scenarios to retest our conviction in the Funds’ energy holdings:

For the liquidity stress tests mentioned previously, we included an even-worse scenario that contemplated nine months of oil at $16, before rising to $30.

While it is hard to know for certain, we believe the probability of the $60 case materializing is higher than the $45 case, which, in turn, is higher than the $30 case. Our analysis of multiple combinations of different supply and demand scenarios suggests that currently large oil supply inventories will likely draw down after 2020, which is positive for oil prices.

Demand Should Return Once Economic Activity Resumes

Since current demand is more a function of health and safety than price, we recognize that future demand will be driven by the timing of a global vaccine deployment. The global scientific community is aggressively working on COVID-19 treatments and vaccines. We forecast demand by end use and think about how long it takes to recover to pre-COVID-19 levels of 100 Mbpd. We estimate this will occur sometime between the end of 2021 and 2023. Longer term, we expect demand to resume its prior trajectory of modest growth, driven by population and GDP growth.

Transportation accounts for the majority of global demand. Passenger vehicle traffic should rebound as economies reopen, as evidenced by early data from China. Longer term, such demand could even exceed prior trends if people continue to avoid public transit. Commercial vehicle traffic has been relatively resilient as trucks continue to carry freight. Air traffic is a wildcard and will likely be the slowest category to recover; however, one third of air traffic is driven by commercial freight and military use, which should remain steady. In addition, petrochemicals are a meaningful source of demand and could increase as oil-based chemicals improve their cost position relative to natural gas-based chemicals at these prices.

There are secular headwinds to higher oil demand, including more employees working from home and teleconferencing. While the return to business travel is hard to forecast, it will likely also be tied to the success of a COVID-19 vaccine.

We believe the “energy transition,” including the shift to electric vehicles (EV), will take longer than expected and not meaningfully alter oil demand over the next few years. In 2019, EVs accounted for 2.6% of global car sales and about 1% of the one billion global passenger vehicles on the world's roads. Longer-term substitution risk is a function of declining battery costs, government mandates to phase out internal combustion engines, and the development of charging infrastructure. We expect that EV penetration will play out slowly without meaningful replacement of passenger vehicle traffic fueled by oil over our investment horizon.

Supply Has Adjusted Quickly to the Decline in Demand

OPEC+7 has agreed to cut output to support oil prices. Significant supply shut-ins (production caps) have resulted in smaller than expected inventory builds, and it is possible that some of that shut-in production is never brought back. Going forward, we think major supply changes will come from two categories: large global producers that have increased production over the past decade and politically driven suppliers. The prolific global supply provinces that have been key contributors to supply over time (Saudi Arabia, Russia, Iraq, and the United States) have further potential to grow, but their rate of growth depends on the oil price. Politically driven suppliers (Iran, Libya, and Venezuela) may be large contributors or detractors of supply depending on geopolitical conditions and policies. For the industry as a whole, new project approvals have largely stopped and are unlikely to restart until oil prices are sustainably higher. We believe oil prices need to rise above $50 to incentivize growth investments. At the current futures curve, our bottom-up research suggests supply will increase gradually from 2020 levels.

4) Finding Value Through Individual Security Selection

Energy is not a homogeneous sector—it includes diverse sub-industries and companies with unique growth prospects and challenges (including technological and project-specific issues), and differing sensitivities to commodity prices. The Funds’ energy investments are diversified across business models and geographies.

We look beyond macro concerns to unearth long-term value opportunities through rigorous bottom-up analysis and individual security selection. As part of our investment process,we assess many factors, including ESG factors, for their potential to materially impact a company’s risk-reward profile.

When evaluating energy stocks, we look for companies with assets that are on the low end of the global cost curve, management teams that have deployed capital prudently through the cycle, and low-to-reasonable valuations. We continue to find compelling long-term opportunities in selected upstream and oilfield services companies with these characteristics, such as those highlighted below.

Concho Resources

Concho Resources is an oil and natural gas exploration and production company that operates primarily in the Permian Basin of Southeast New Mexico and West Texas. The company is trading at an inexpensive valuation despite its low-cost and large resource base that should allow the company to have moderate growth with meaningful free cash flow generation over a number of years. Concho Resources has a resilient balance sheet. It has no debt maturities until 2025 and a flexible capital program that allows Concho to adjust capital expenditures down to align with its operating cash flow. The company also entered the downturn with limited financial leverage. From an operating perspective, at $30 oil, production likely declines at a low single digit rate. In the $40s, production can be held flat. At $50+ oil, Concho can grow production at mid-single digits with growing free cash flow generation. Management has a conservative reputation, and its interests are well aligned with long-term shareholders.

Hess

Hess, an independent oil and gas exploration and production company, is investing its strong cash flows from existing assets into a new project with significant production potential in Guyana. The company owns 30% of a partnership with Exxon Mobil in the Stabroek block in Guyana, which is one of the largest oil discoveries in recent decades and one of the lowest-cost projects outside of OPEC. Much of the Stabroek block remains unexplored, and Hess has interests in additional blocks in Guyana and neighboring Suriname. Incremental discoveries on these blocks could provide additional upside. Higher incremental returns from this investment should result in attractive free cash flow growth over the next several years.

Hess’ management team has expressed a desire to return free cash flow to shareholders. While the Guyana resource will require significant capital over the next several years and Hess is reliant on solid execution from Exxon, we believe these risks are manageable. Trading at eight times cash flow, Hess is an attractive investment opportunity.

In Closing

We are enthusiastic about the long-term outlook for the Dodge & Cox Worldwide Funds’ energy investments. Our global industry and fixed income credit analysts have rigorously stress tested the financial models for each of the Funds’ energy holdings, and we believe the companies have sufficient capital and liquidity to navigate the challenging market environment and deliver longterm value to shareholders. Furthermore, we have extensively assessed the macro environment and company-specific risks, and believe the valuations of our carefully selected holdings remain attractive.

Patience and persistence are essential to long-term investment success. We encourage our clients and shareholders to take a similar view. Thank you for your continued confidence in Dodge & Cox.

Disclosures

This information should not be considered a solicitation or an offer to purchase shares of Dodge & Cox Worldwide Funds plc or a solicitation or an offer by Dodge & Cox Worldwide Investments and its affiliates to provide any services in any jurisdiction. The views expressed herein represent the opinions of Dodge & Cox Worldwide Investments and its affiliates and are not intended as a forecast or guarantee of future results for any product or service. To obtain more information about the Funds, please refer to the Funds' prospectus at dodgeandcoxworldwide.com.

The above information is not a complete analysis of every material fact concerning any market, industry, or investment. Data has been obtained from sources considered reliable, but Dodge & Cox makes no representations as to the completeness or accuracy of such information. Opinions expressed are subject to change without notice.

The information provided is historical and does not predict future results or profitability. This is not a recommendation to buy, sell, or hold any security and is not indicative of Dodge & Cox’s current or future trading activity. Any securities identified are subject to change without notice and do not represent a Fund’s entire holdings.

The MSCI EAFE (Europe, Australasia, Far East) Index is a broad-based, unmanaged equity market index aggregated from 21 developed market country indices. The MSCI World Index is a broad-based, unmanaged equity market index aggregated from 23 developed market country indices, including the United States and Canada. The MSCI ACWI (All Country World Index) Index is a broad-based, unmanaged equity market index aggregated from 46 developed and emerging market country indices. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This publication is not approved, reviewed, or produced by MSCI.

The S&P 500 Index is a market capitalization-weighted index of 500 large capitalization stocks commonly used to represent the U.S. equity market. The S&P 500 Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Dodge & Cox. Copyright 2020 S&P Dow Jones Indices LLC, a division of S&P Global, Inc. and/or its affiliates.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance, L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. The Bloomberg Barclays U.S. Aggregate Bond Index is a widely recognized, unmanaged index of U.S. dollar-denominated, investment-grade, taxable fixed income securities. The Bloomberg Barclays Global Aggregate Bond Index is a widely recognized, unmanaged index of multi-currency, investment-grade fixed income securities.

Endnotes

1 As of 30 June 2020. Dodge & Cox Stock Fund (% of Fund’s net assets): Apache (0.7%), Baker Hughes (1.4%), Concho Resources (1.0%), Halliburton (0.7%), Hess (1.0%), National Oilwell Varco (0.4%), Occidental Petroleum (2.3%), Schlumberger (1.1%), and The Williams Companies (0.7%). Dodge & Cox International Stock Fund (% of Fund’s net assets): Equinor (1.4%), Ovintiv (0.7%), Schlumberger (1.4%), Suncor Energy (2.2%), and Total (2.3%). Dodge & Cox Global Stock Fund (% of Fund’s net assets): Apache (0.7%), Baker Hughes (0.8%), Hess (0.8%), Occidental Petroleum (1.8%), Ovintiv (0.7%), Schlumberger (0.9%), and Suncor Energy (1.5%). Dodge & Cox Income Fund (% of Fund’s net assets): Exxon Mobil (0.9%), Kinder Morgan (1.1%), Occidental Petroleum (0.5%), Petroleo Brasileiro (Petrobras, 0.8%), Petroleos Mexicanos (PEMEX, 2.1%), Rio Oil Finance Trust (1.0%), TC Energy (1.7%), The Williams Companies (0.2%), and Ultrapar Participacoes (0.5%). Dodge & Cox Global Bond Fund (% of Fund’s net assets): Concho Resources (1.0%), EOG Resources (0.3%), Exxon Mobil (0.5%), Kinder Morgan (1.7%), Occidental Petroleum (1.0%), Petroleo Brasileiro (Petrobras, 1.2%), Petroleos Mexicanos (PEMEX, 1.7%), Rio Oil Finance Trust (0.8%), TC Energy (2.2%), The Williams Companies (0.7%), and Ultrapar Participacoes (0.8%). Dodge & Cox Balanced Fund (% of Fund’s net assets): Apache (0.4%), Baker Hughes (1.0%), Concho Resources (0.6%), Exxon Mobil (0.1%), Halliburton (0.5%), Hess (0.7%), Kinder Morgan (0.3%), National Oilwell Varco (0.2%), Occidental Petroleum (1.7%), Petroleo Brasileiro (Petrobras, 0.1%), Petroleos Mexicanos (PEMEX, 0.5%), Rio Oil Finance Trust (0.4%), Schlumberger (0.7%), TC Energy (0.4%), The Williams Companies (0.7%), and Ultrapar Participacoes (0.2%).

2 The Organization of the Petroleum Exporting Countries (OPEC) is an intergovernmental organization of 13 nations. The current OPEC members are Algeria, Angola, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, the Republic of the Congo, Saudi Arabia (the de facto leader), the United Arab Emirates, and Venezuela.

3 All returns are stated in U.S. dollars unless otherwise noted.

4 Unless otherwise specified, all weightings and characteristics are as of 30 June 2020.

5 Numbers are based on 31 March 2020 consolidated financial statements with pro-forma adjustments for known debt issuance and maturities during the second quarter of 2020.

6 The use of specific examples does not imply that they are more or less attractive investments than the portfolio’s other holdings.

7 OPEC plus countries (OPEC+) include the 13 members of OPEC and the following 10 additional oil exporting countries (led by Russia): Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Russia, South Sudan, and Sudan.